REV Group has had an impressive run over the past six months as its shares have beaten the S&P 500 by 6.3%. The stock now trades at $30.85, marking a 20.5% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy REV Group, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.Despite the momentum, we don't have much confidence in REV Group. Here are three reasons why REVG doesn't excite us and a stock we'd rather own.

Why Is REV Group Not Exciting?

Offering the first full-electric North American fire truck, REV (NYSE:REVG) manufactures and sells specialty vehicles.

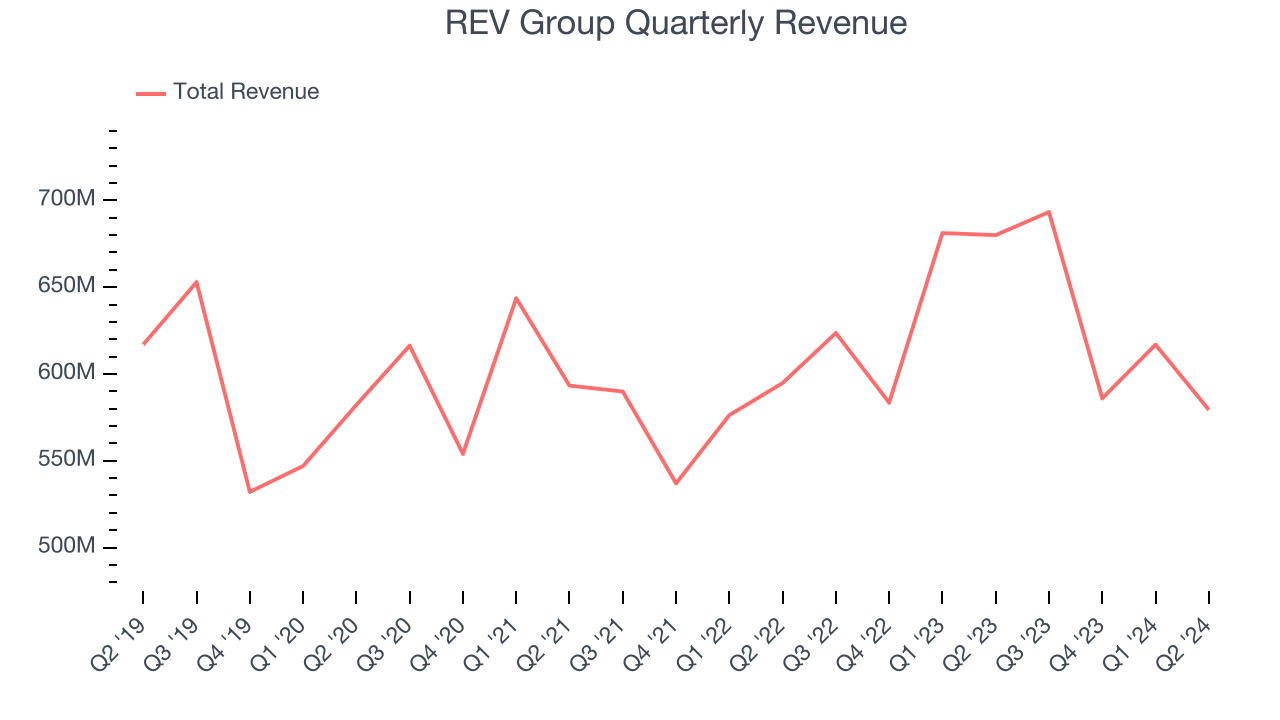

1. Long-Term Revenue Growth Flatter Than a Pancake

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, REV Group struggled to consistently increase demand as its $2.48 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a lower quality business.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect REV Group’s revenue to stall, a deceleration versus its 3.8% annualized growth for the past two years. This projection is underwhelming and implies its products and services will face some demand challenges.

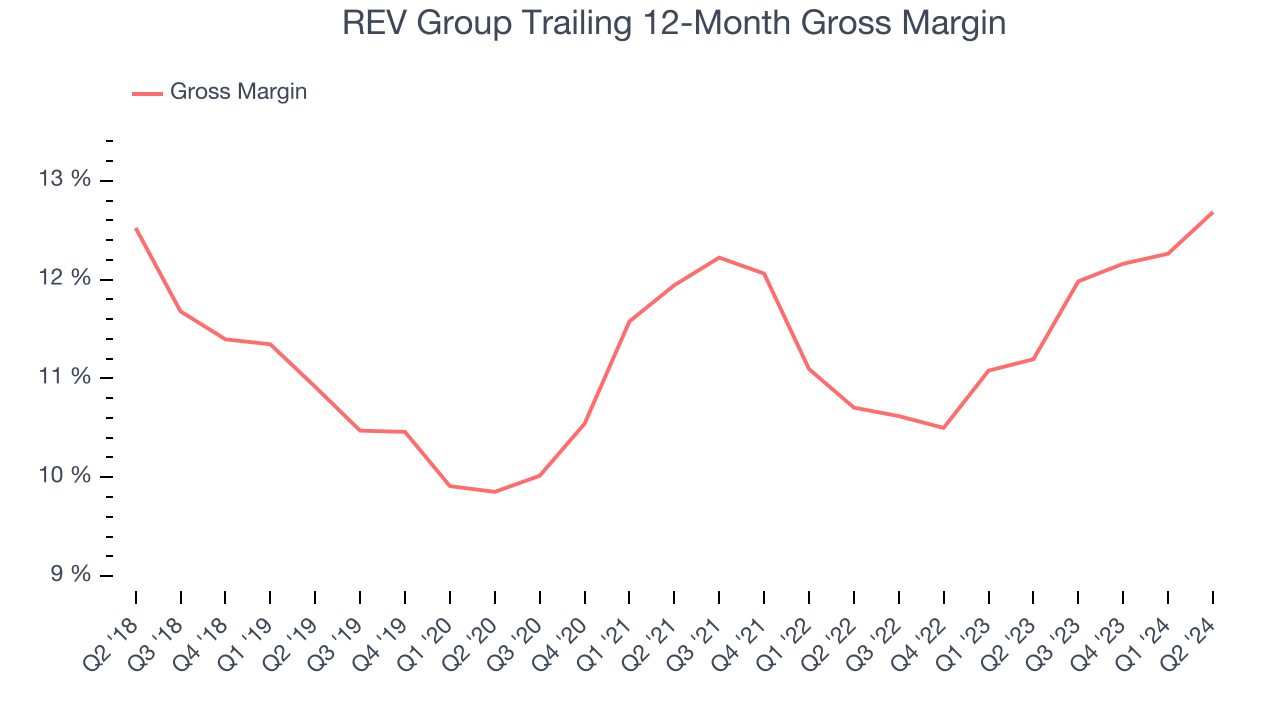

3. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

REV Group has poor unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 11.3% gross margin over the last five years. That means REV Group paid its suppliers a lot of money ($88.70 for every $100 in revenue) to run its business.

Final Judgment

REV Group isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 15.6x forward price-to-earnings (or $30.85 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d recommend looking at Google, whose cloud computing and YouTube divisions are firing on all cylinders.

Stocks We Would Buy Instead of REV Group

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.