Texas Instruments currently trades at $200.25 per share and has shown little upside over the past six months, posting a middling return of 2.7%. The stock also fell short of the S&P 500’s 14.2% gain during that period.

Is now the time to buy Texas Instruments, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.We're swiping left on Texas Instruments for now. Here are three reasons why you should be careful with TXN and a stock we'd rather own.

Why Is Texas Instruments Not Exciting?

Headquartered in Dallas, Texas since the 1950s, Texas Instruments (NASDAQ:TXN) is the world’s largest producer of analog semiconductors.

1. Long-Term Revenue Growth Disappoints

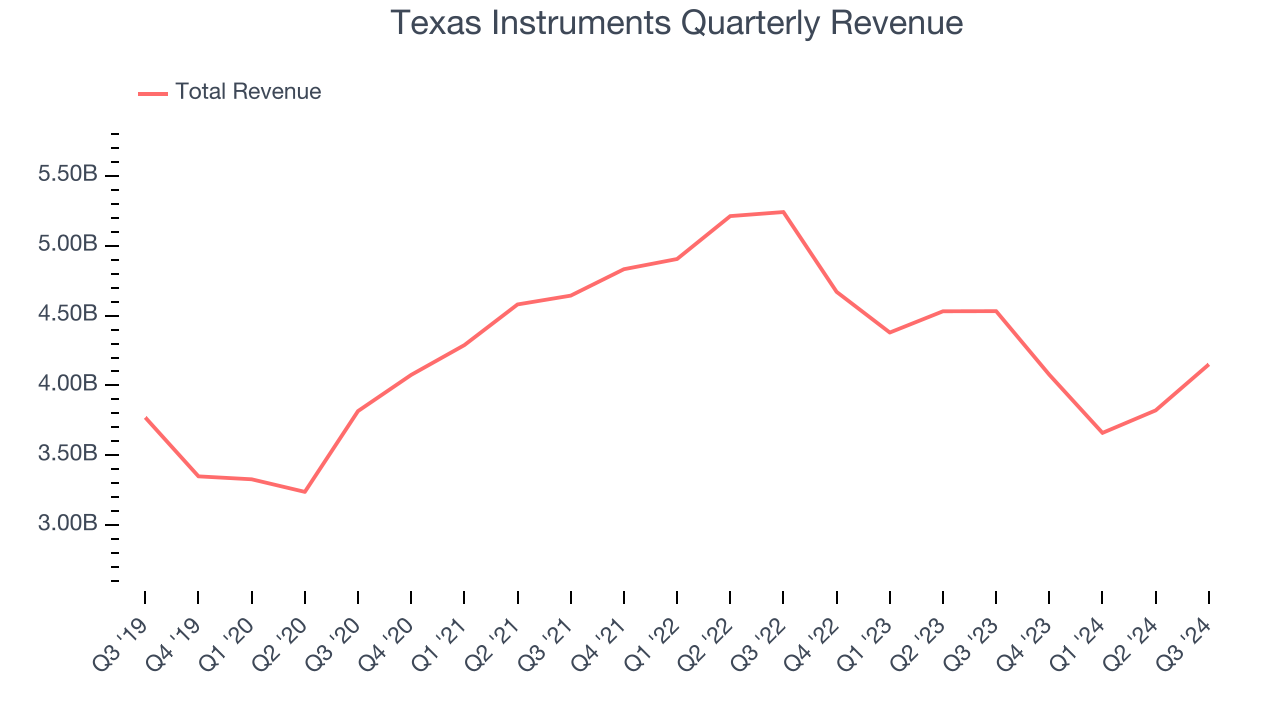

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Texas Instruments’s 1.3% annualized revenue growth over the last five years was weak. This fell short of our benchmarks. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

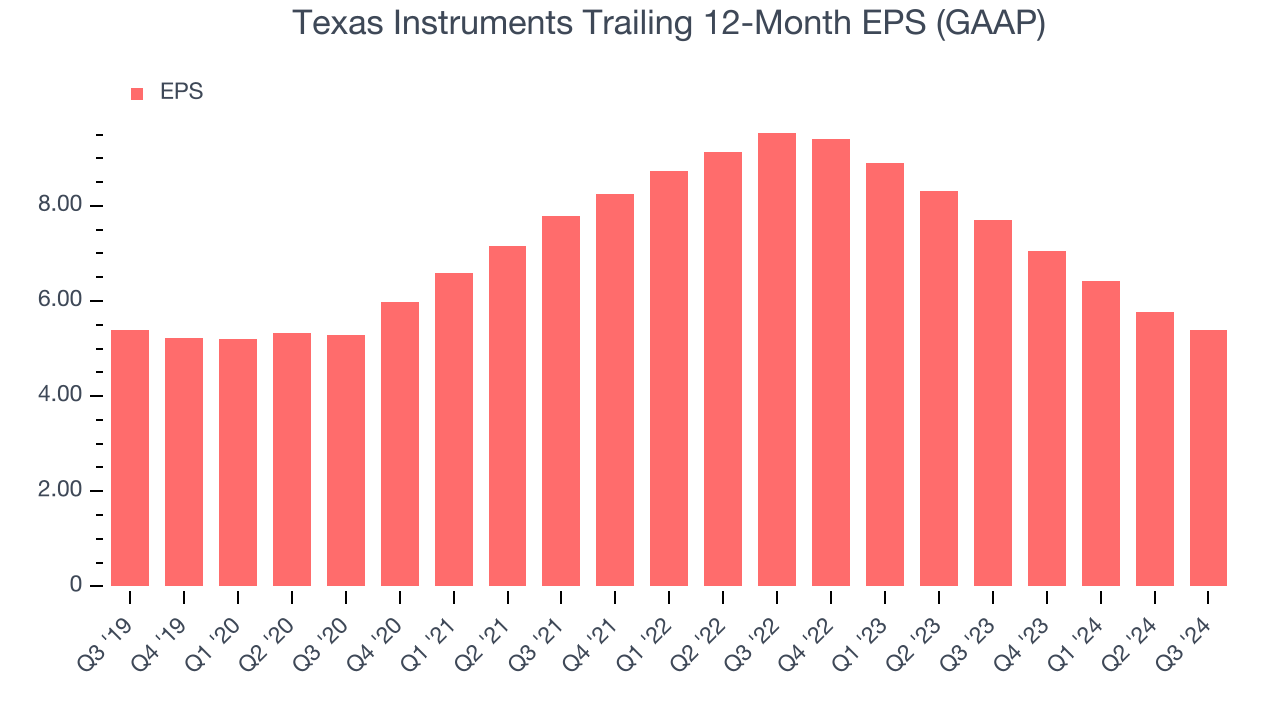

2. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Texas Instruments’s flat EPS over the last five years was below its 1.3% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

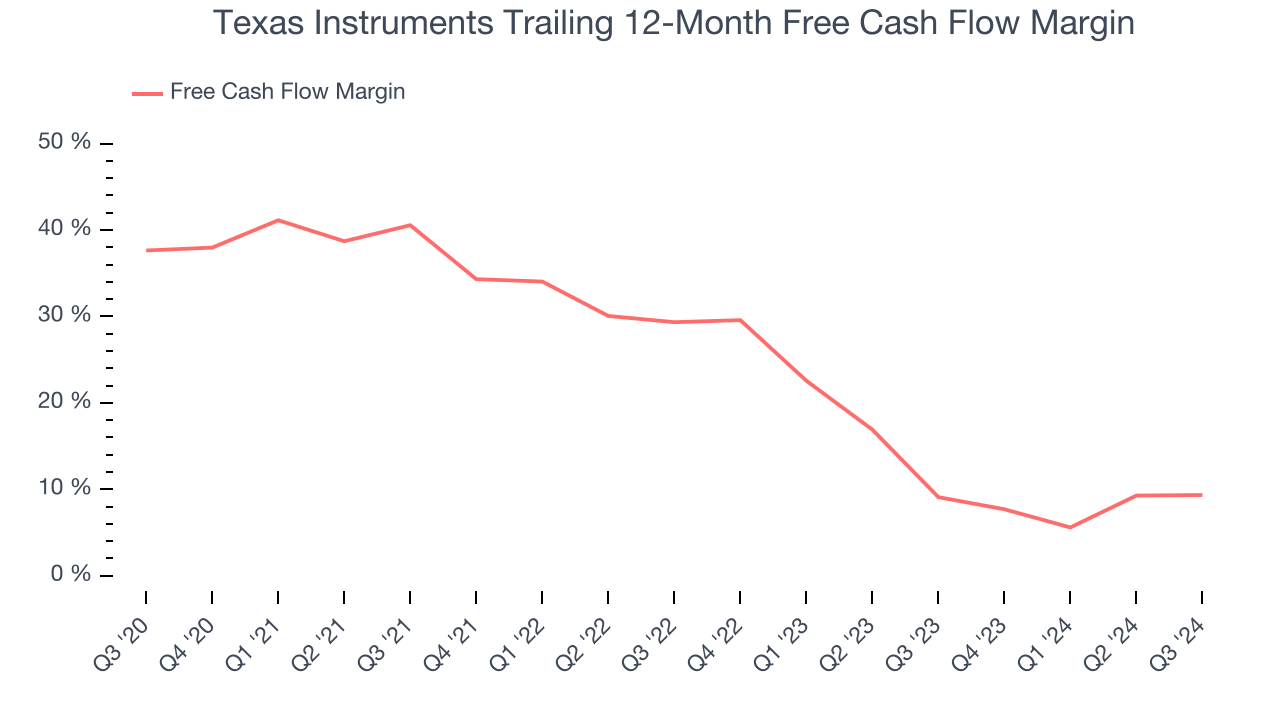

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Texas Instruments’s margin dropped by 28.3 percentage points over the last five years. If this trend continues, it could signal it’s becoming a more capital-intensive business. Texas Instruments’s free cash flow margin for the trailing 12 months was 9.3%.

Final Judgment

Texas Instruments’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 32.2x forward price-to-earnings (or $200.25 per share). This valuation tells us a lot of optimism is priced in - we think there are better investment opportunities out there. We’d recommend looking at Wabtec, a leading provider of locomotive services benefiting from an upgrade cycle.

Stocks We Like More Than Texas Instruments

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.