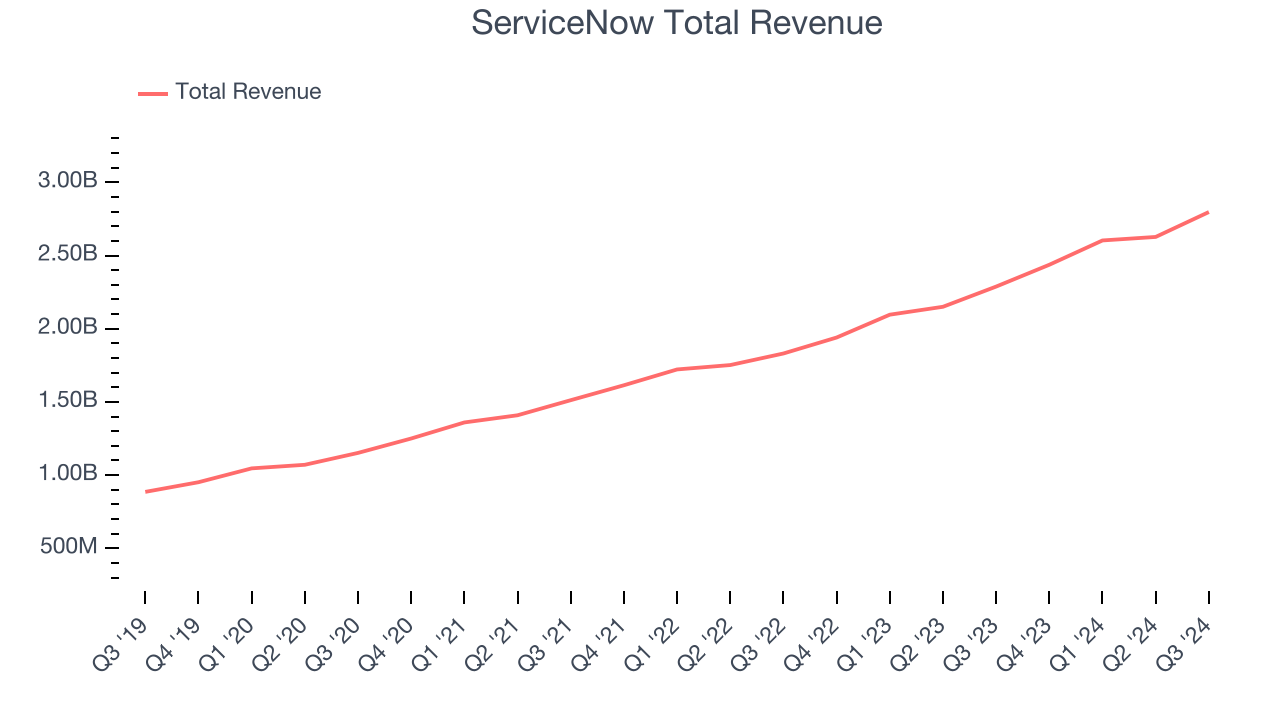

Enterprise workflow software maker ServiceNow (NYSE:NOW) reported Q3 CY2024 results exceeding the market’s revenue expectations, with sales up 22.2% year on year to $2.80 billion. Its non-GAAP profit of $3.72 per share was also 7.8% above analysts’ consensus estimates.

Is now the time to buy ServiceNow? Find out by accessing our full research report, it’s free.

ServiceNow (NOW) Q3 CY2024 Highlights:

- Revenue: $2.80 billion vs analyst estimates of $2.75 billion (1.9% beat)

- Adjusted EPS: $3.72 vs analyst estimates of $3.45 (7.8% beat)

- Subscription Revenue Guidance for Q4 CY2024 is $2.88 billion at the midpoint, slightly above analyst estimates of $2.86 billion

- Gross Margin (GAAP): 79.1%, in line with the same quarter last year

- Operating Margin: 14.9%, up from 10.1% in the same quarter last year

- Free Cash Flow Margin: 16.8%, up from 13.6% in the previous quarter

- Customers: 2,020 customers paying more than $1m annually

- Current RPO (remaining performance obligations): $9.36 billion vs analyst estimates of $9.11 billion (2.7% beat)

- Market Capitalization: $189 billion

“ServiceNow raised our full year topline guidance on the strength of our Q3 results, once again going beyond expectations,” said ServiceNow Chairman and CEO Bill McDermott.

Company Overview

Founded by Fred Luddy, who wrote the code for the company's initial prototype on a flight from San Francisco to London, ServiceNow (NYSE:NOW) offers a software-as-a-service platform that helps companies become more efficient by allowing them to automate workflows across IT, HR, and customer service.

Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Luckily, ServiceNow’s sales grew at a decent 23.7% compounded annual growth rate over the last three years. This shows it was successful in expanding, a useful starting point for our analysis.

This quarter, ServiceNow reported robust year-on-year revenue growth of 22.2%, and its $2.80 billion of revenue topped Wall Street estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 19.8% over the next 12 months, a deceleration versus the last three years. Some tapering is natural given the magnitude of its revenue base, and we still think its growth trajectory is attractive.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

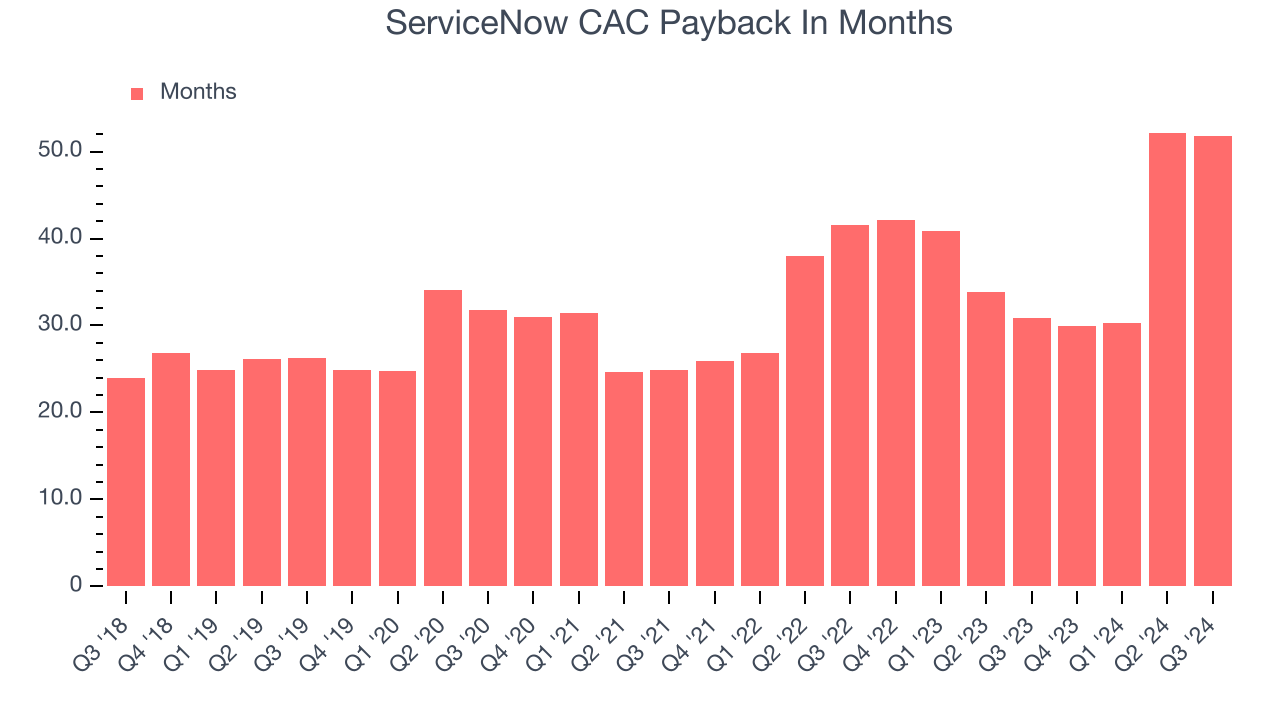

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly the business can break even on its sales and marketing investments.

It’s relatively expensive for ServiceNow to acquire new customers as its CAC payback period checked in at 51.8 months this quarter. The company’s performance indicates that it operates in a competitive market and must continue investing to maintain its growth trajectory.

Key Takeaways from ServiceNow’s Q3 Results

It was encouraging to see ServiceNow narrowly top analysts’ revenue expectations this quarter. Additionally, current RPO (remaining performance obligations), a leading indicator of future revenues, came in ahead. Looking ahead, its subscription revenue guidance for next quarter came in ahead. Overall, this was a fine quarter. However, the stock traded down 1.3% to $896 immediately after reporting.

ServiceNow’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.