Over the past six months, EnerSys’s shares (currently trading at $92.22) have posted a disappointing 11.4% loss, well below the S&P 500’s 9.7% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in EnerSys, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why ENS doesn't excite us and a stock we'd rather own.

Why Is EnerSys Not Exciting?

Supplying batteries that power equipment as big as mining rigs, EnerSys (NYSE:ENS) manufactures various kinds of batteries for a range of industries.

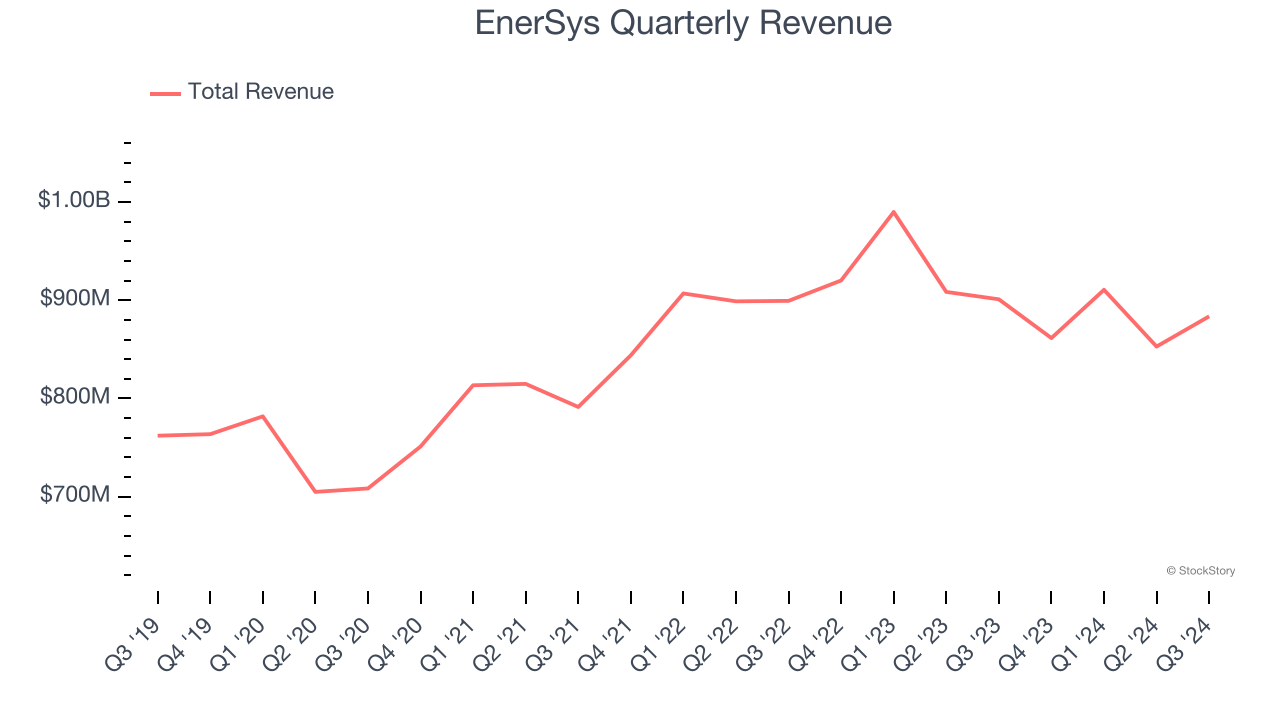

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, EnerSys’s sales grew at a sluggish 3.1% compounded annual growth rate over the last five years. This was below our standard for the industrials sector.

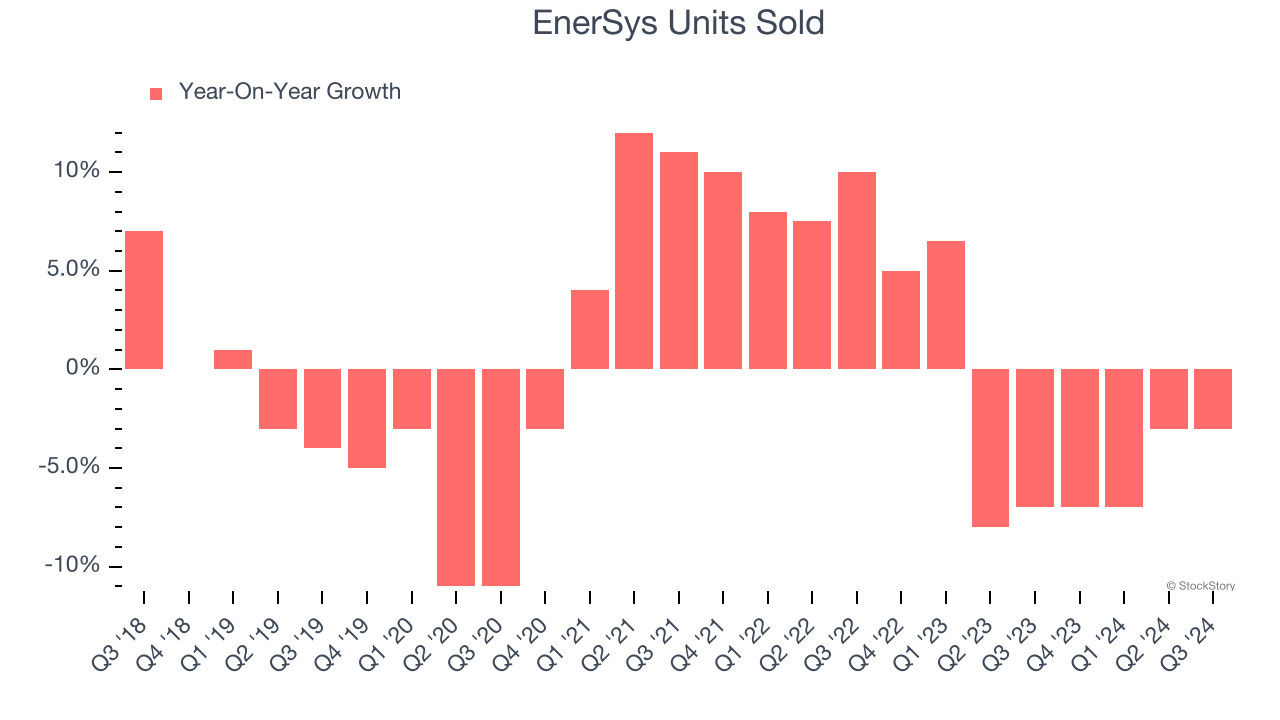

2. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Renewable Energy company because there’s a ceiling to what customers will pay.

Over the last two years, EnerSys’s units sold averaged 2.9% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests EnerSys might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

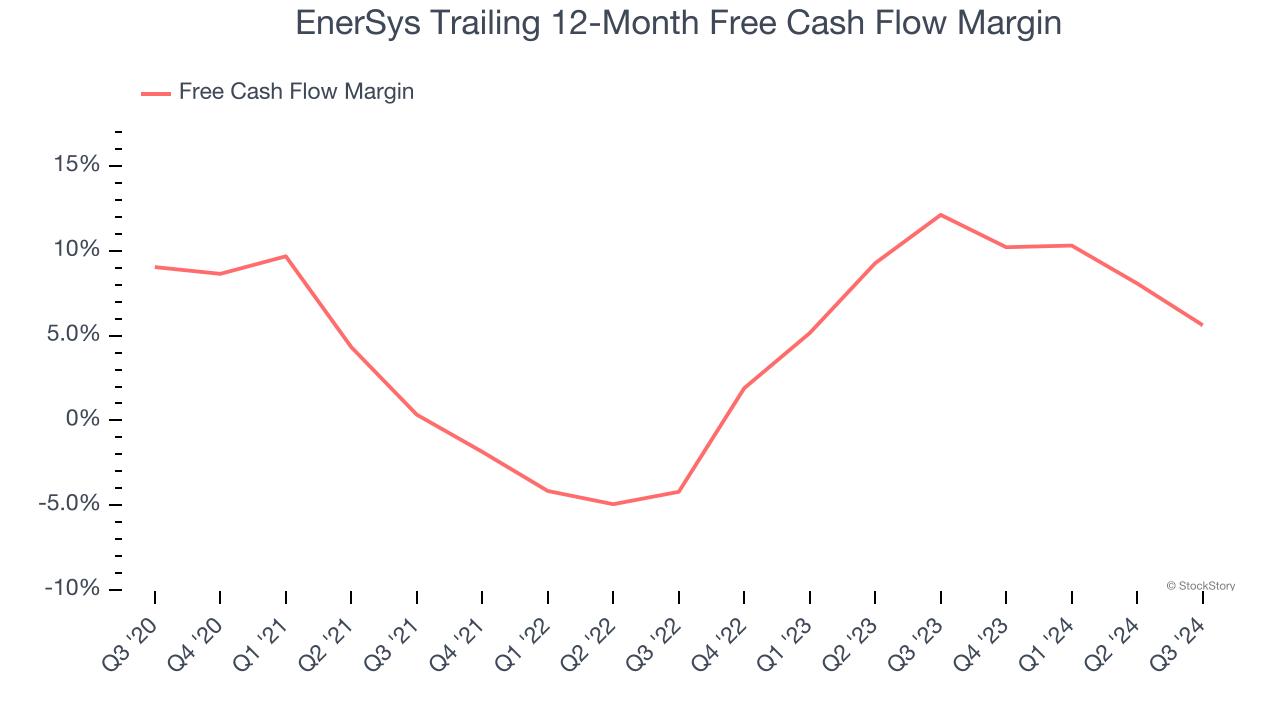

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, EnerSys’s margin dropped by 3.4 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. EnerSys’s free cash flow margin for the trailing 12 months was 5.6%.

Final Judgment

EnerSys isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 9.9× forward price-to-earnings (or $92.22 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at Yum! Brands, an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than EnerSys

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.