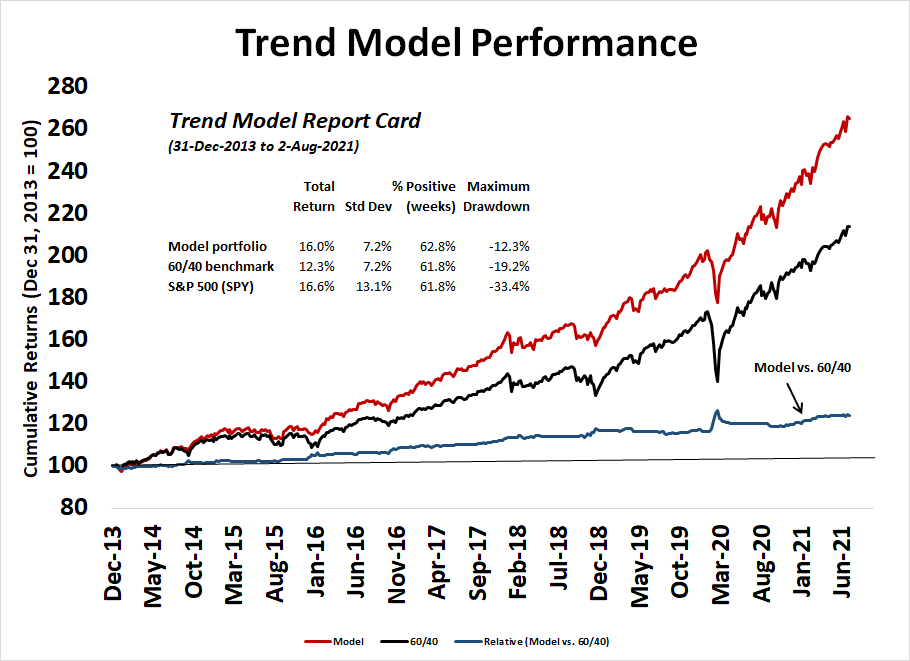

The Trend Asset Allocation Model is an asset allocation model that applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. The performance and full details of a model portfolio based on the out-of-sample signals of the Trend Model can be found here.

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don't buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the email alerts is updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities*

- Trend Model signal: Bullish*

- Trading model: Neutral*

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of those email alerts is shown here.

Subscribers can access the latest signal in real-time here.

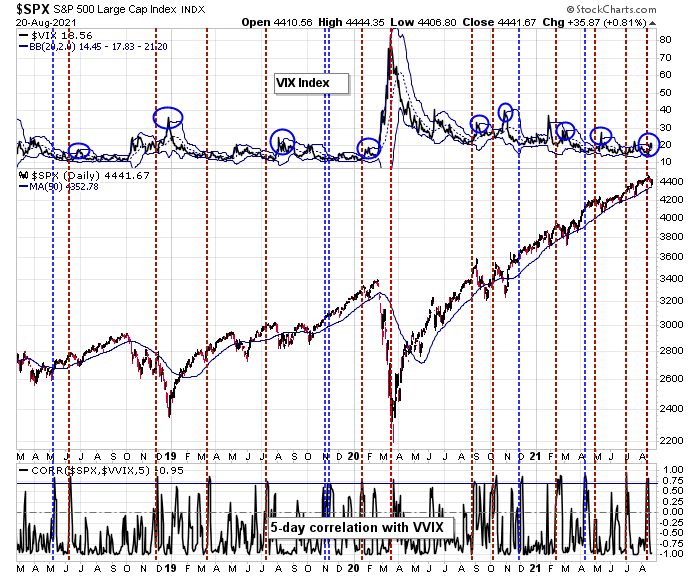

A risk-off episodeA week ago, I highlighted the risk of stock market weakness because the correlation between the S&P 500 and VVIX, or the volatility of the VIX, had spiked. The pullback duly arrived and the S&P 500 briefly tested its 50 dma.

In the past, S&P 500 and VVIX correlation spike sell signal sell-offs have bottomed when the VIX Index spiked above its upper Bollinger Band. Barring a new and unexpected shock, market internals have sufficiently deteriorated that a short-term bottom is near.

If I am right in my tactical assessment, the minor panic last week was just a brief summer squall.

The full post can be found here.