Reemphasizes Need for the Board to Immediately Repay Debt and Refinance RYAM’s 2024 Senior Notes

Chatham Asset Management, LLC, a private investment firm which manages funds that beneficially own approximately 6.3% of the outstanding common stock of Rayonier Advanced Materials (“RYAM” or the “Company”) (NYSE: RYAM) and is a substantial bondholder of the Company, today issued an open letter to RYAM shareholders reaffirming its intention to withhold its vote against two long-tenured members of the Company’s Board of Directors, Thomas I. Morgan and Lisa M. Palumbo, at the Company’s annual meeting of shareholders on May 16, 2022.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20220509005337/en/

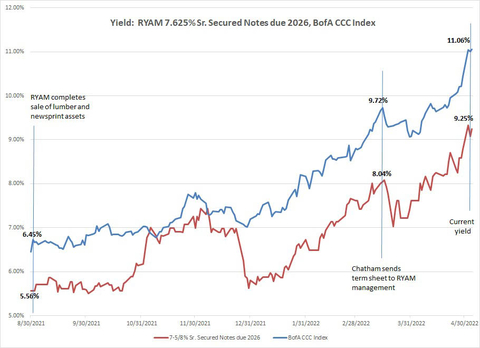

Yield: RYAM 7.625% Sr. Secured Notes due 2026, BofA CCC Index (Source: Bloomberg; Bank of America HY Index)

The full text of the letter follows:

May 9, 2022

Dear Fellow Shareholders:

Chatham Asset Management, LLC (together with its affiliates, “we” or “Chatham”) is a substantial stockholder and bondholder of Rayonier Advanced Materials (“RYAM” or the “Company”), beneficially owning approximately 6.3% of the Company’s outstanding common stock, 77% of the Company’s 5.50% Senior Notes due June 1, 2024 (the “2024 Notes”), and 13% of the Company’s 7.625% Senior Secured Notes due January 15, 2026 (the “2026 Notes”).

On April 13, 2022, we wrote an open letter to shareholders detailing the reasons for why we intend to withhold our votes against two long-tenured members of the Company’s Board of Directors (the “Board”), Thomas I. Morgan and Lisa M. Palumbo, at the Company’s annual meeting of shareholders on May 16, 2022 (the “Annual Meeting”). In that letter, we expressed our view that a withhold vote against Mr. Morgan and Ms. Palumbo is warranted, not only to show that this Board must be held accountable for years of shareholder value destruction, but also for their incredible entrenchment maneuver in adopting a poison pill without shareholder approval, despite having the ability to allow shareholders to vote on it at the Annual Meeting. We also expressed serious concerns with the Company’s strategy in waiting to address the refinancing of the 2024 Notes in light of weakening credit markets and rising interest rates.

Since issuing that letter, the following has occurred, which further supports our decision to withhold our votes against Mr. Morgan and Ms. Palumbo:

1. A leading proxy advisor firm, Institutional Shareholder Services Inc. (“ISS”), is recommending that shareholders vote AGAINST the Board’s Nominating and Corporate Governance Committee chair, Lisa Palumbo, at the Annual Meeting for adopting a short-term poison pill with a relatively low 10 percent trigger. In making this recommendation, ISS noted:

“The adoption of a pill can lead to board entrenchment and deter legitimate offers of acquisition,which can ultimately lead to lower long-term shareholder value.”

“Given the potentially vital role a poison pill may have in determining the future of a company, shareholders should have the right to vote on the implementation of all new poison pills, as well as any material changes to existing pills.”

“The company adopted the pill on March 21, 2022, eight weeks before the 2022 annual meeting, and 11 days before filing its definitive proxy statement.”

“[T]he company's share price is down approximately 28.4 percent since the adoption of the pill, closing at $6.79 on March 21, 2022, and $4.86 on May 2, 2022. This is compared to an approximate 7.1 percent decrease in the Russell 3000 over the same time period. Therefore, given the relatively low 10 percent ownership trigger, a vote against governance committee chair Lisa Palumbo is warranted.”

2. Since we first publicly expressed on March 17, 2022, our serious concerns that management was not acting quickly enough to proactively repay its debt with available cash and address the Company’s upcoming debt maturities, market conditions have deteriorated and Federal interest rates have increased. In fact, yields for CCC rated notes like RYAM’s notes, which are the riskiest part of the junk bond market, have widened to 11.06% as of April 30, 2022, from 9.72% when we first sent a proposed exchange offer term sheet at the Company’s request (the “Proposed Term Sheet”), and 6.45% when the Company closed on the sale of its lumber and newsprint assets (the “Asset Sale”). At the same time, yields on the Company’s 2026 Notes have similarly widened to 9.25% versus 8.04% at the time of our Proposed Term Sheet and 5.56% at the time of the Asset Sale.

See Yield: RYAM 7.625% Sr. Secured Notes due 2026, BofA CCC Index chart

3. Since the second quarter of 2021, a period of strong performance in the Company’s lumber business which it has since divested, the Company has been carrying larger than normal amounts of liquidity and cash. Over the last four quarters, the Company’s liquidity position has averaged over $350 million, well above historical levels despite the Asset Sale in August 2021. If the Company had applied some of its cash to debt reduction and maintained historical levels of liquidity, we estimate interest savings of $8 million over the last twelve months. We estimate these savings would be worth approximately $1 per share today, an 18% premium to the Company’s current share price, based on a 10x forward earnings multiple.

4. We note a recently failed deal in the U.S. junk bond primary market this month, as the medical device company Bioventus pulled a $415 million 5-year bond sale, citing poor market conditions despite an indicated yield in the 10% range. In our view, the markets will only get worse, not better, particularly for CCC-rated notes, as Federal interest rates are projected to rise throughout the year, making the Company’s strategy to wait, ill-advised.

While we recently had some engagement with management regarding our concerns, new potential terms for a refinancing and further debt reduction, we were disappointed to hear that the Company continues to believe it can wait for both market conditions and the Company’s operating performance to improve. We find this risk of waiting to be a dangerous strategy further warranting our WITHHOLD votes.

According to the Company’s Corporate Governance Principles, if any director fails to receive the affirmative vote of a majority of the votes cast with regard to his or her election, then such director must tender his or her resignation to the Board. The Board’s Nominating and Corporate Governance Committee would then consider such resignation and make a recommendation to the Board as to whether to accept or decline the resignation. The Board would then make a determination and publicly disclose its decision and rationale within 90 days after receipt of the tendered resignation.

In our view, a WITHHOLD vote against Thomas I. Morgan and Lisa M. Palumbo, who have both served on the Board for eight years, is warranted to send a strong and clear message that the Board should not have defensively and unilaterally adopted a poison pill and must act with speed to address its upcoming debt maturity.

Sincerely,

/s/ Anthony Melchiorre

Anthony Melchiorre

Managing Member

Chatham Asset Management

View source version on businesswire.com: https://www.businesswire.com/news/home/20220509005337/en/

Contacts

Jonathan Gasthalter/Sam Fisher

Gasthalter & Co.

(212) 257-4170