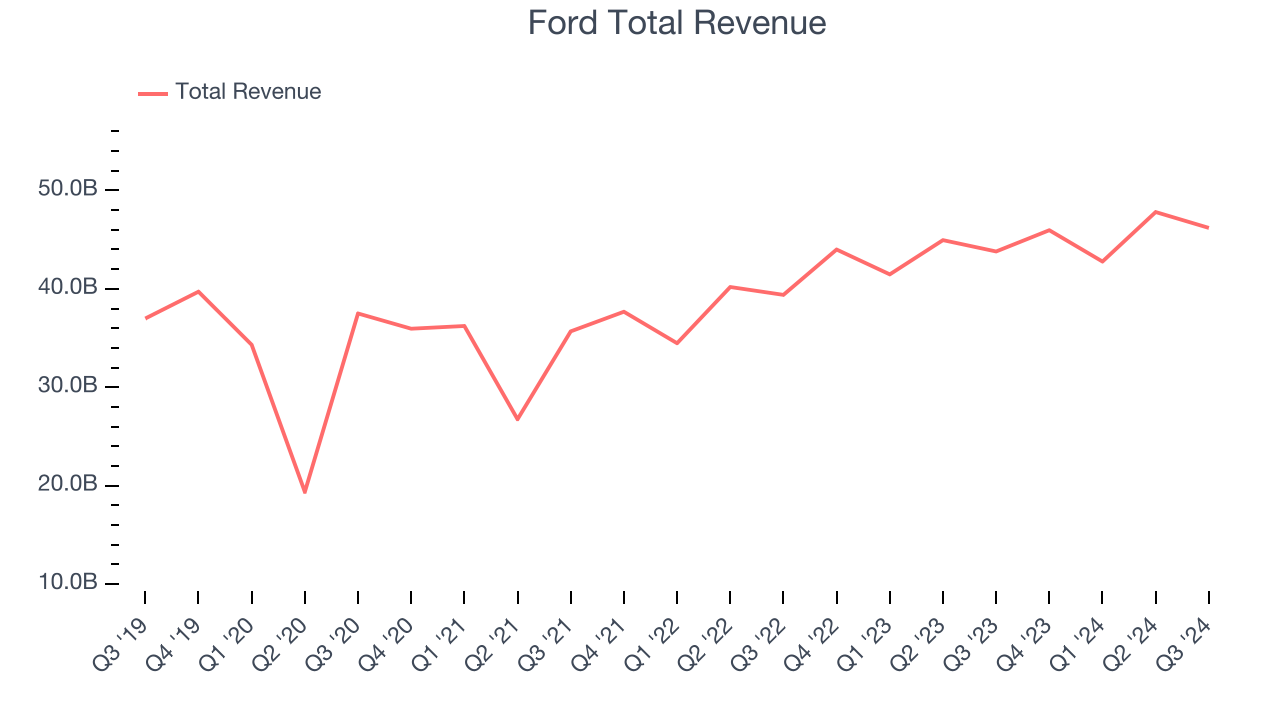

Automotive manufacturer Ford (NYSE:F) announced better-than-expected revenue in Q3 CY2024, with sales up 5.5% year on year to $46.2 billion. Its non-GAAP profit of $0.49 per share was also 3.5% above analysts’ consensus estimates.

Is now the time to buy Ford? Find out by accessing our full research report, it’s free.

Ford (F) Q3 CY2024 Highlights:

- Revenue: $46.2 billion vs analyst estimates of $42.32 billion (9.1% beat)

- Adjusted EPS: $0.49 vs analyst estimates of $0.47 (3.5% beat)

- Gross Margin (GAAP): 13%, up from 9.1% in the same quarter last year

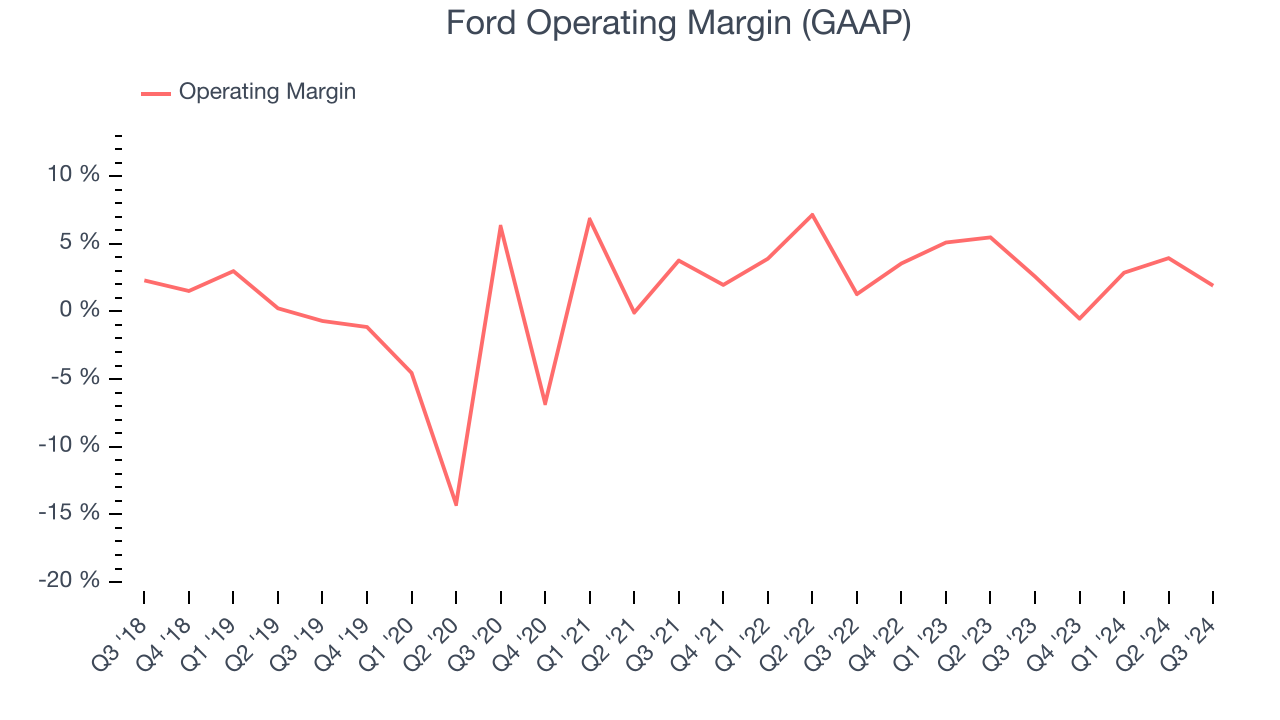

- Operating Margin: 1.9%, in line with the same quarter last year

- Free Cash Flow Margin: 7.6%, up from 5.4% in the same quarter last year

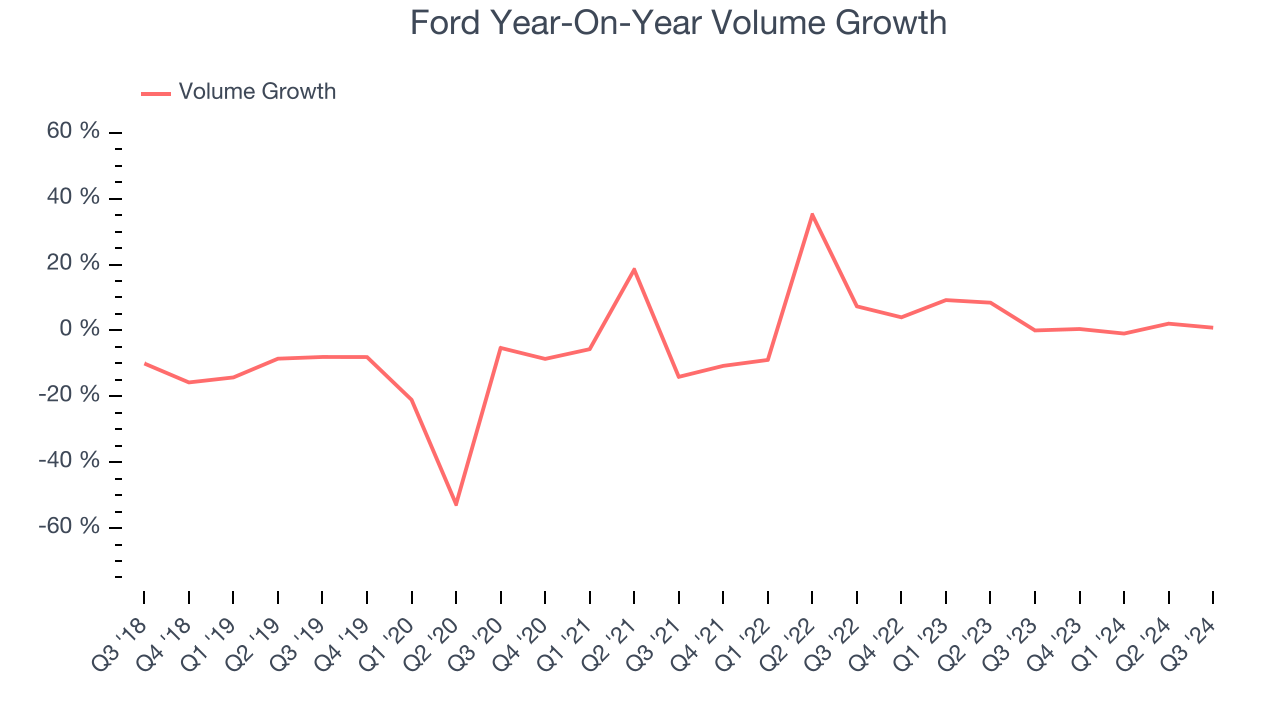

- Sales Volumes were flat year on year, in line with the same quarter last year

- Market Capitalization: $44.01 billion

Company Overview

Established to make automobiles accessible to a broader segment of the population, Ford (NYSE:F) designs, manufactures, and sells a variety of automobiles, trucks, and electric vehicles.

Automobile Manufacturers

Much capital investment and technical know-how are needed to manufacture functional, safe, and aesthetically pleasing automobiles for the mass market. Barriers to entry are therefore high, and auto manufacturers with economies of scale can boast strong economic moats. However, this doesn’t insulate them from new entrants, as electric vehicles (EVs) have entered the market and are upending it. This has forced established manufacturers to not only contend with emerging EV-first competitors but also decide how much they want to invest in these disruptive technologies, which will likely cannibalize their legacy offerings.

Sales Growth

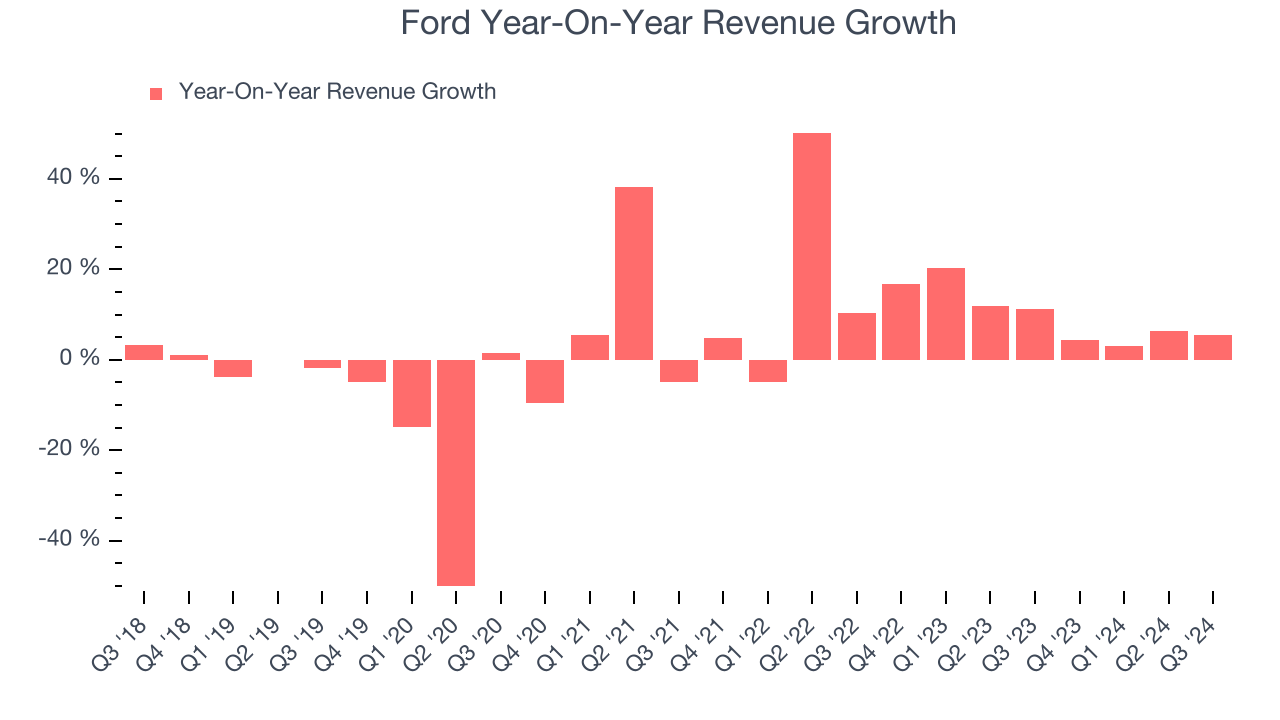

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Regrettably, Ford’s sales grew at a sluggish 3% compounded annual growth rate over the last five years. This shows it failed to expand in any major way, a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Ford’s annualized revenue growth of 9.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its sales volumes, which reached 1.1 million in the latest quarter. Over the last two years, Ford’s sales volumes averaged 3% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Ford reported year-on-year revenue growth of 5.5%, and its $46.2 billion of revenue exceeded Wall Street’s estimates by 9.1%.

Looking ahead, sell-side analysts expect revenue to decline 3.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and illustrates the market thinks its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Ford was profitable over the last five years but held back by its large cost base. Its average operating margin of 2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the bright side, Ford’s annual operating margin rose by 3.9 percentage points over the last five years.

This quarter, Ford generated an operating profit margin of 1.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

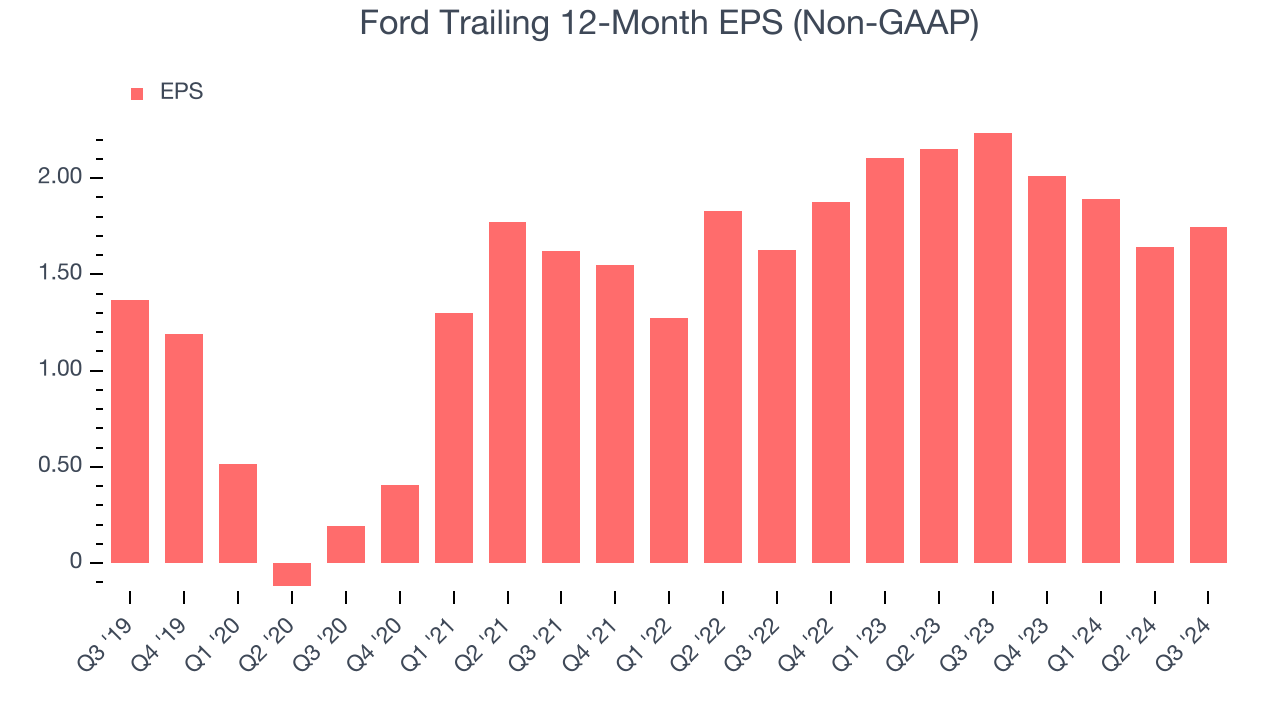

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Ford’s EPS grew at an unimpressive 5% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 3% annualized revenue growth and tells us the company became more profitable as it expanded.

We can take a deeper look into Ford’s earnings to better understand the drivers of its performance. As we mentioned earlier, Ford’s operating margin was flat this quarter but expanded by 3.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Ford, its two-year annual EPS growth of 3.5% was lower than its five-year trend. We hope its growth can accelerate in the future.In Q3, Ford reported EPS at $0.49, up from $0.39 in the same quarter last year. This print beat analysts’ estimates by 3.5%. Over the next 12 months, Wall Street expects Ford’s full-year EPS of $1.75 to grow by 8.8%.

Key Takeaways from Ford’s Q3 Results

We were impressed by how much Ford blew past analysts’ revenue and EPS expectations this quarter. On the other hand, its sales volumes missed. Overall, this quarter had some key positives, but the market seemed to focus on the weaker-than-anticipated sales volumes. The stock traded down 5% to $10.81 immediately after reporting.

Should you buy the stock or not?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.